Claims cycle time is one of the most important metrics in a storm restoration roofing operation — and one of the least tracked. Most owners know their close rate. Some track their average settlement value. Almost none have a clear picture of how long their claims are taking to move from filing to final settlement, or what that timeline is actually costing them.

That gap is expensive. And fixing it starts with understanding what claims cycle time actually is, what a reasonable benchmark looks like, and what actually moves it.

The Definition

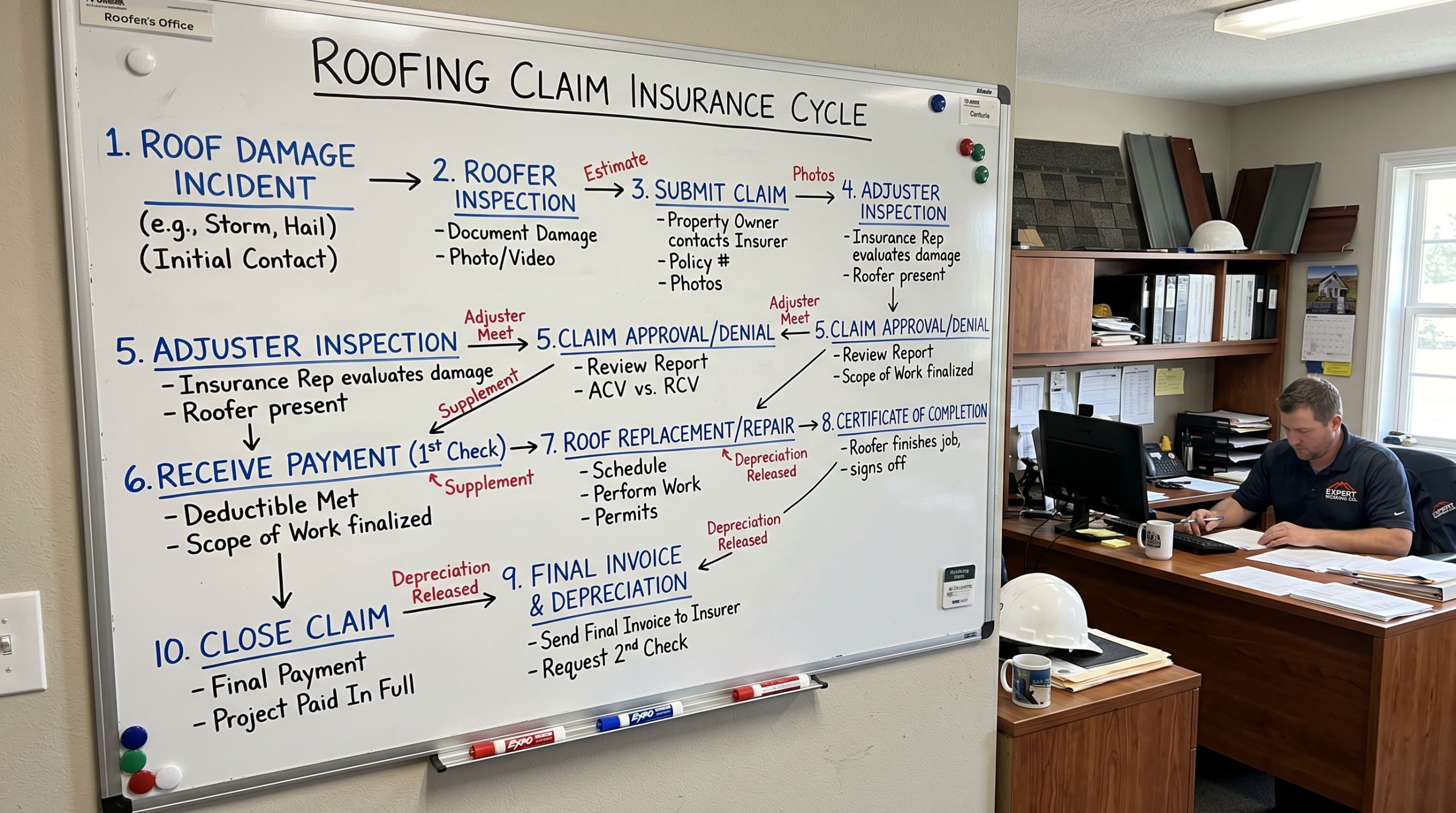

Claims cycle time is the number of days between when a claim is filed and when it reaches final settlement. It measures how efficiently a claim moves through the full process — from initial filing, through the coverage decision, through negotiation and supplementing, to the point where the homeowner’s claim is fully resolved and the contractor can complete the job.

In storm restoration roofing, cycle time is a direct measure of process health. A well-run claims process produces consistent, predictable cycle times. A fractured, rep-dependent process produces wildly variable ones — some claims closing in weeks, others dragging for months with no clear reason why.

Why Cycle Time Matters Beyond Cash Flow

The most obvious impact of long cycle times is cash flow. When claims take 90 days instead of 45, the revenue tied to those jobs sits longer before landing. For a high-volume operation running a large open pipeline at any given time, that delay has real financial consequences — on payroll, on overhead decisions, and on the owner’s ability to plan with confidence.

But cycle time affects more than cash flow.

Claims that drag lose leverage. The longer a file sits without resolution, the more the advantage shifts toward the insurance company. Follow-up becomes harder. Documentation requests get more complex. Supplements that would have been straightforward to negotiate at 30 days become contentious at 90. The claim that should have closed cleanly becomes a drawn-out back-and-forth — and often settles for less than it would have with tighter cycle management.

Homeowners also feel cycle time. A homeowner whose claim is still open after three months is not a happy homeowner — regardless of how the claim eventually resolves. That experience affects referrals, reviews, and the contractor’s reputation in a market they’re trying to grow.

What a Reasonable Benchmark Looks Like

Cycle time varies by market, carrier, claim complexity, and how contested the claim is. There’s no single universal number that applies to every job. But there are patterns worth understanding.

A straightforward claim — clear damage, cooperative carrier, complete initial file — should move from filing to settlement in the range of 30 to 60 days when the process is managed actively. Claims that involve supplements, carrier pushback, or appraisal add time, but even contested claims should have a defined path forward rather than sitting indefinitely.

When claims in a portfolio are regularly stretching past 90 days without a clear reason, that’s a red flag — not about the carriers or the market, but about the process managing those files. Stale claims are almost always a process problem before they’re a carrier problem.

What Actually Moves Cycle Time

The factors that compress cycle time are almost entirely process-driven:

File quality at the start. A complete, well-documented claim file gives the adjuster what they need to make a decision faster. Incomplete files generate requests for additional information, which adds days or weeks to the timeline before the process can move forward.

Active follow-up. Claims don’t move on their own. Every stage of the process requires someone to be actively pushing it forward — following up on pending decisions, responding to carrier requests, tracking where each file stands and what it needs next. In a rep-dependent operation, that follow-up happens when the rep has time. In a standardized process, it happens on schedule.

Early supplement identification. Supplements pursued proactively — identified and submitted as part of the standard process rather than as an afterthought — resolve faster and with less friction than supplements raised late. When the supplement process is built into the claims lifecycle from the start, it compresses rather than extends the overall timeline.

Clear ownership at every stage. Claims stall when nobody knows who’s responsible for the next step. When every stage of the process has a defined owner and a defined timeline, files move because they have to — not because someone happened to remember.

The Bottom Line

Claims cycle time is a measurement of how well a claims process actually works. Consistent, predictable cycle times are the output of a standardized process. Variable, unpredictable ones are the output of a process that depends on individual people managing files their own way.

Tracking cycle time — and understanding what’s driving it — is one of the clearest windows into the health of a claims operation. For most high-volume storm restoration companies, that window reveals more room for improvement than they expected.

Frequently Asked Questions

What is claims cycle time in storm restoration roofing?

Claims cycle time is the number of days between when a claim is filed and when it reaches final settlement. It measures how efficiently a claim moves through the full process and is one of the most direct indicators of claims process health. Consistent, short cycle times reflect a well-run process. Variable, extended ones reflect a process that depends on individual people rather than a standardized system.

What is a normal claims cycle time for a storm restoration roofing company?

A straightforward claim with a complete initial file and a cooperative carrier should move from filing to settlement in the range of 30 to 60 days under active process management. Claims regularly stretching past 90 days without a clear reason are almost always a process problem before they’re a carrier problem.

What causes long claims cycle times in roofing insurance restoration?

The most common causes are incomplete initial files that generate carrier requests for additional information, lack of active follow-up at each stage of the process, supplements identified and submitted late rather than proactively, and unclear ownership of who’s responsible for moving each file forward. All of these are process problems — correctable with the right infrastructure in place.

Why Roofing Contractors Outsource Claims: Compliance Is Part of the Reason

YVA is a done-for-you claims infrastructure platform for high-volume storm restoration roofing companies. We’re not attorneys and this isn’t legal advice but we’ve built our process around having licensed professionals own the activities that require a license. Learn more at YourVirtualAdjuster.com.

Comments