If you asked ten roofing company owners to define a claim file, you’d get ten different answers. Some would describe it as the paperwork. Some would say it’s the estimate. Some would reference the photos. A few would struggle to define it at all — which is part of the problem.

A claim file isn’t any one of those things. It’s all of them together, organized in a specific way, for a specific purpose. And how well that file is built from the start is one of the most direct determinants of how a claim performs from coverage decision through final settlement.

The Definition

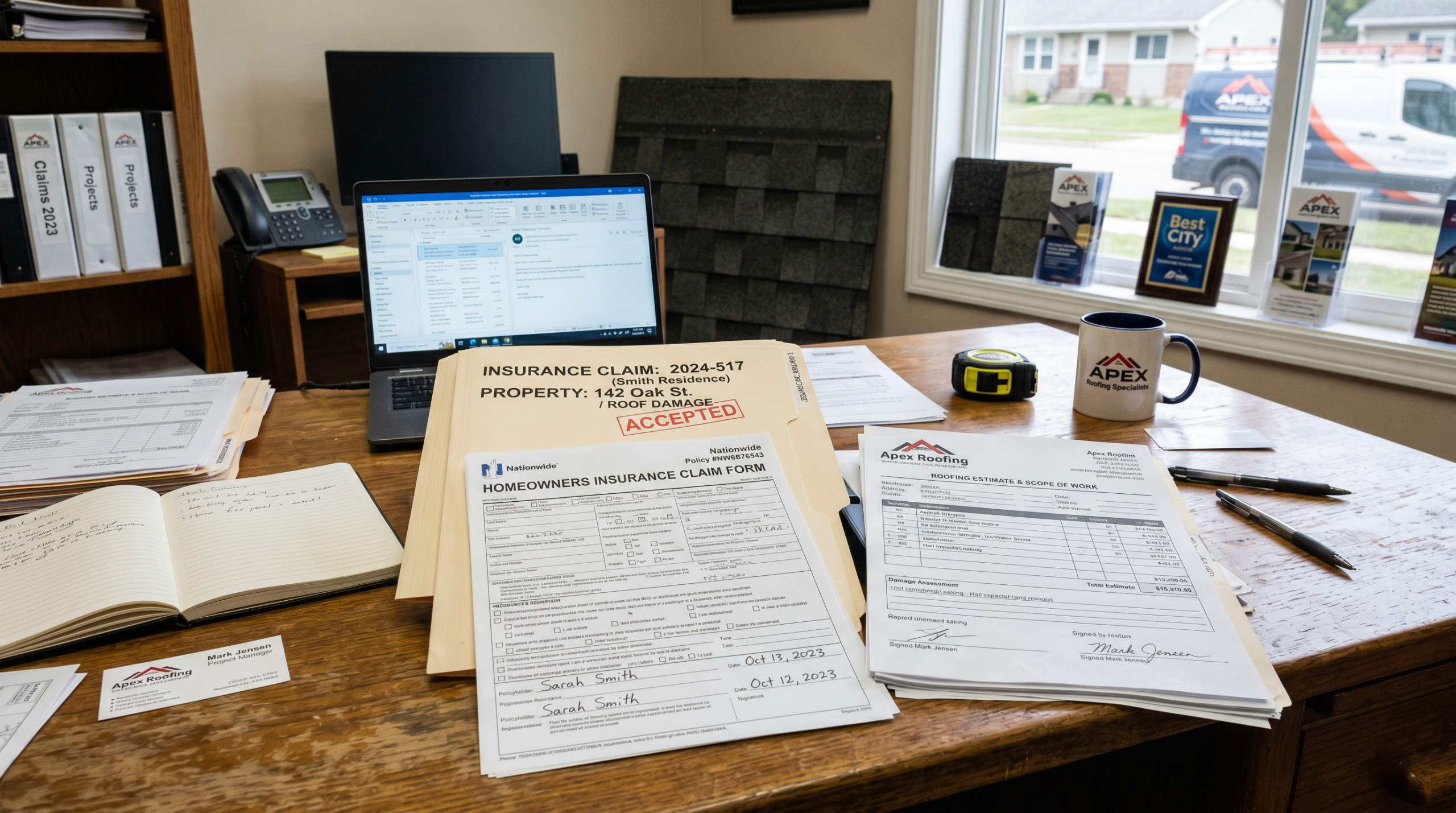

A claim file is the documentation package that presents and supports an insurance claim — and sets it up correctly for the long term. It is the case being made: the evidence, the scope, and the supporting materials that establish what damage exists, what it will cost to repair, and why that cost is justified.

How the file is built at the start directly determines the reserve the insurance company sets. That reserve becomes the anchor for everything that follows — negotiation, supplementing, and final settlement. A file that establishes the full picture of the damage from day one sets a reserve that reflects the actual value of the claim. A file with gaps sets a low reserve that’s difficult and costly to recover from at every subsequent stage.

In storm restoration roofing, a claim file typically includes:

**The estimate.** A detailed, line-by-line scope of the work required to restore the property to its pre-loss condition. This is the financial argument of the claim. A thin or incomplete estimate produces a thin approval.

**The photo report.** Documented photographic evidence of the damage — organized, labeled, and thorough enough to show the adjuster exactly what exists on that property and why it supports the scope being claimed.

**Supporting documentation.** Weather verification reports, one-click code reports, manufacturer specs, inspection reports, and any other material that independently supports the damage assessment and the scope of loss. This is what separates a claim that gets approved at full value from one that gets pushed back.

Why File Quality Matters More Than Most Contractors Realize

The claim file isn’t administrative paperwork. It’s the case for the claim.

Insurance companies make coverage and settlement decisions based on what’s in front of them. A well-built file tells a complete story — the damage is documented, the scope is supported, the cost is justified, and every line item has a basis. A poorly built file leaves gaps that adjusters fill with lower numbers, and gaps that are hard to recover from once a reserve is set.

This is why the quality of the initial file — not just whether it gets filed, but how completely and accurately it gets built — has an outsized impact on everything that follows. A strong file sets a fair reserve. A fair reserve makes negotiation easier. Easier negotiation means less friction on supplements. Less friction means faster cycle times and better outcomes.

The file quality effect compounds in both directions. A strong file from day one creates momentum. A weak file from day one creates resistance at every subsequent stage.

What a Broken Claims Process Does to File Quality

In a rep-dependent claims model, file quality is inconsistent — and in most cases, it’s not being built by the rep at all. What typically happens is the rep meets the adjuster, the insurance company produces their own scope, and the rep works from whatever the carrier puts out. There’s no independently built file, no proactive documentation package, no effort to establish the full picture of the damage before the carrier sets their number.

That means the reserve gets set entirely on the insurance company’s terms — based on their adjuster’s assessment, with no competing documentation to anchor it higher. Everything that follows is a negotiation from a position the contractor never had a hand in shaping.

The problem isn’t that reps are building files poorly. It’s that in most operations, a properly built claim file doesn’t exist at all going into the adjuster meeting. The carrier’s scope becomes the starting point by default and from that point forward, everything is a reaction to a number the contractor had no part in setting.

A standardized claims infrastructure changes that dynamic entirely. The file gets built before the adjuster meeting, not after. The damage is documented, the scope is supported, and the reserve gets anchored to the actual value of the claim — not whatever the carrier’s adjuster happened to write down. Every file, every time, regardless of who sold the job.

The Bottom Line

A claim file is the foundation of every insurance claim in storm restoration. How it’s built — and whether it gets built at all before the adjuster meeting — determines how the claim performs from that point forward.

In most rep-dependent operations, the carrier sets the terms and the contractor reacts to them. In a standardized claims infrastructure, the file gets built first, the reserve gets anchored correctly, and the claim moves forward from a position that was shaped by the process — not handed to it by the insurance company.

Frequently Asked Questions

What is a claim file in roofing insurance restoration?

A claim file is the documentation package that presents and supports an insurance claim — the estimate, photo report, and supporting documentation that establishes what damage exists, what it costs to repair, and why. It needs to exist before the adjuster meeting, not after. How it’s built from the start directly determines the reserve the insurance company sets, which anchors everything that follows through final settlement.

Why does claim file quality matter for storm restoration roofing companies?

Insurance companies make settlement decisions based on what’s in the file. A well-built file sets a fair reserve and creates momentum through every subsequent stage — negotiation, supplementing, and final settlement. A poorly built file sets a low reserve that’s hard to recover from and creates resistance at every stage that follows.

How does claims infrastructure improve claim file quality for roofing companies?

In most rep-dependent operations, a properly built claim file doesn’t exist going into the adjuster meeting — the carrier produces their own scope and the contractor reacts to it. A standardized claims infrastructure changes that by building the file first, anchoring the reserve to the actual value of the damage, and ensuring every claim starts from a position the process shaped — not one the insurance company handed down.

Why Roofing Contractors Outsource Claims: Compliance Is Part of the Reason

YVA is a done-for-you claims infrastructure platform for high-volume storm restoration roofing companies. We’re not attorneys and this isn’t legal advice but we’ve built our process around having licensed professionals own the activities that require a license. Learn more at YourVirtualAdjuster.com.

Comments